The International Trade Blog ![]() International Sales & Marketing

International Sales & Marketing

Methods of Payment in International Trade: Letters of Credit

On: October 14, 2024 | By:  David Noah |

12 min. read

David Noah |

12 min. read

One of the most important considerations when it comes to international trade is how you are going to get paid for your exports. While relying on cash upfront may eliminate the risk of non-payment, it limits your universe of potential customers as it can cause cash flow and other problems for buyers.

There are five primary methods of payment in international trade that range from most to least secure: cash in advance, letter of credit, documentary collection or draft, open account and consignment. Of course, the most secure method for the exporter is the least secure for the importer and vice versa. The key is to strike the right balance for both sides. This article focuses on letters of credit (LCs).

What Is a Letter of Credit in Global Trade?

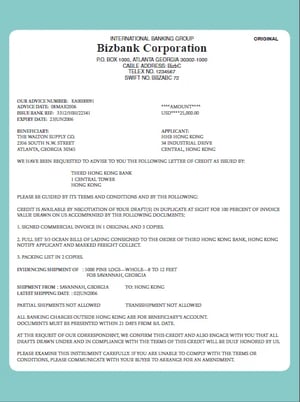

A letter of credit, also referred to as a documentary credit, is a contractual agreement whereby the issuing bank (importer's bank), acting on behalf of the customer (the importer or buyer), promises to make payment to the beneficiary or exporter against the receipt of complying stipulated documents. The issuing bank will typically use intermediary banks to facilitate the transaction and make payment to the exporter.

Understanding a Letter of Credit

Understanding a Letter of Credit

The LC is a separate contract from the sales contract on which it is based; therefore, banks are not concerned with the quality of the underlying goods or whether each party fulfills the terms of the sales contract.

The bank's obligation to pay is solely conditioned upon the seller's compliance with the terms and conditions of the LC. In LC transactions, banks deal in documents only, not goods.

LCs can be arranged easily for one-time transactions between the exporter and importer or used for an ongoing series of transactions.

A letter of credit may be irrevocable, which means that it cannot change unless both parties agree; or, it can be revocable, in which case either party may unilaterally make changes. Unless the conditions of the LC state otherwise, it is always irrevocable, which means the document may not be changed or canceled unless the importer, banks and exporter agree. A revocable LC is inadvisable, as it carries many risks for the exporter.

The Advantages of a Letter of Credit

LCs are one of the most versatile and secure instruments available to international traders. Since LCs are credit instruments, the importer's credit with their bank is used to obtain an LC. The importer pays the bank a fee to render this service. An LC is useful when reliable credit information about a foreign buyer is difficult to obtain or if the foreign buyer's credit is unacceptable, but the exporter is satisfied with the creditworthiness of the importer's bank.

This method also protects the importer because the documents required to trigger payment provide evidence that goods have been shipped as agreed. However, because LCs open up the potential for discrepancies, which may negate payment to the exporter, documents should be prepared by trained professionals.

Discrepant documents—literally not having an "i dotted and t crossed"—may negate the bank's payment obligation. That's why many export companies use export documentation and compliance software like Shipping Solutions to ensure their export paperwork is accurate and complete.

Confirmed Letter of Credit

A greater degree of protection is afforded to the exporter when an LC issued by a foreign bank (the importer's issuing bank) is confirmed by a U.S. bank.

The exporter asks its customer to have the issuing bank authorize a bank in the exporter's country to confirm (this bank is typically the advising bank, which then becomes the confirming bank). Confirmation means that the U.S. bank adds its engagement to pay the exporter to that of the foreign bank. If an LC is not confirmed, the exporter is subject to the payment risk of the foreign bank and the political risk of the importing country.

Exporters should consider getting confirmed LCs if they are concerned about the credit standing of the foreign bank or when they are operating in a high-risk market where political upheaval, economic collapse, devaluation or exchange controls could put the payment at risk. Exporters should also consider getting confirmed LCs when importers are asking for extended payment terms.

The Letter of Credit Process

There are typically seven steps that occur to get paid using a letter of credit:

- The importer arranges for the issuing bank to open an LC in favor of the exporter.

- The issuing bank transmits the LC to the nominated bank, which forwards it to the exporter.

- The exporter forwards the goods and documents to a freight forwarder.

- The freight forwarder dispatches the goods and either the dispatcher or the exporter submits documents to the nominated bank.

- The nominated bank checks documents for compliance with the LC and collects payments from the issuing bank for the exporter.

- The importer's account at the issuing bank is debited.

- The issuing bank releases documents to the importer to claim the goods from the carrier and to clear them at customs.

Parties to a Letter of Credit

While an LC usually involves the exporter, importer and both parties' banks, these four principals can be referred to by different names:

- Applicant—The importer (foreign buyer).

- Beneficiary—The exporter (seller).

- Issuing Bank—Importer's bank that opens the LC in favor of the exporter.

- Nominating Bank—Exporter's bank that facilitates the eventual payment from the importer's bank.

- Advising Bank—Exporter's bank that informs the beneficiary of the opening of the LC and verifies its authenticity.

- Confirming Bank—Exporter's bank that adds its own guarantee to pay if the importer's bank fails to do so.

- Exporter's Bank—Generally the exporter will ask that their own bank be used by the importer's bank as (1) an advising bank and (2) a confirming bank. The advising bank is normally also given the nominated bank's role.

Special Letters of Credit

Letters of credit can take many forms. When an LC is made transferable, the payment obligation under the original LC can be transferred to one or more second beneficiaries. With a revolving LC, the issuing bank restores the credit to its original amount each time it is drawn down.

A standby LC is not intended to serve as the means of payment for goods but can be drawn in the event of a contractual default, including the failure of an importer to pay invoices when due. Similarly, standby LCs are often posted by exporters in favor of an importer because they can serve as bid bonds, performance bonds and advance payment guarantees. In addition, standby LCs are often used as counter guarantees against the provision of down payments and progress payments on the part of foreign buyers.

Tips For Exporters on Using Letters of Credit

If you’re considering letters of credit for your exports, keep these things in mind:

- Banks pay only the amount specified in the LC, even if higher charges for shipping, insurance or other factors are incurred and documented.

- Consult with your bank before the importer applies for an LC to determine if an LC is appropriate for the transaction, what the costs will be and how disputes are resolved.

- Consider whether a confirmed LC is needed.

- Upon receiving an LC, carefully compare the letter’s terms with the terms of the proforma invoice. This is extremely important because the terms must be precisely met or the LC may be invalid (and you may not get paid). If meeting the terms is impossible, or any documented information is even slightly incorrect, contact the customer immediately and ask for an amendment.

- Negotiate with the buyer and agree on detailed terms to be incorporated into the LC. You may request that the LC specify that partial shipments and trans-shipment will be allowed. Specification can prevent unforeseen problems.

- Determine if all LC terms can be met within the prescribed time limits. Provide documentation showing goods were shipped by the date specified in the LC.

- Ensure all documents are consistent with the terms and conditions of the LC.

- Be cautious of discrepancy opportunities that may delay or cause non-payment.

Like what you read? Join thousands of exporters and importers who subscribe to Passages: The International Trade Blog. You'll get the latest news and tips for exporters and importers delivered right to your inbox.

This article is taken in large part from the Trade Finance Guide: A Quick Reference for U.S. Exporters, which you can download for free by clicking the link below.